Have you ever looked at a credit bureau report on yourself? A credit bureau report can provide you with information that you need to make yourself look as good as possible, financially, on paper. In the hectic world we live in today, people often rely on credit. You may need credit to buy a car, buy a house, get a credit card to buy clothes, and so many other things.

Many people have very little credit information on record, and others have had some mistakes in the past and some negative marks on their credit bureau report that they need to correct in order to maximize their abilities to borrow money.

A credit bureau report can be acquired simply by contacting any of the three major credit reporting agencies. A new federal law requires them to give you one credit bureau report per year at no charge. In the past you always had to pay for these reports, so this new law works to the benefit of the consumer.

Getting your free credit bureau report is so important that every consumer should take advantage of it and check out what the credit bureau report has to say about them on an annual basis.

When you see your credit bureau report it might seem a bit confusing if you haven’t read one in the past. While the information it contains is confidential, you can find a financial professional that you trust, sit down with him and let him explain the information on the credit bureau report to you so that you can utilize it to the maximum. The credit bureau report is your personal information, and by using it you can improve your own personal financial status.

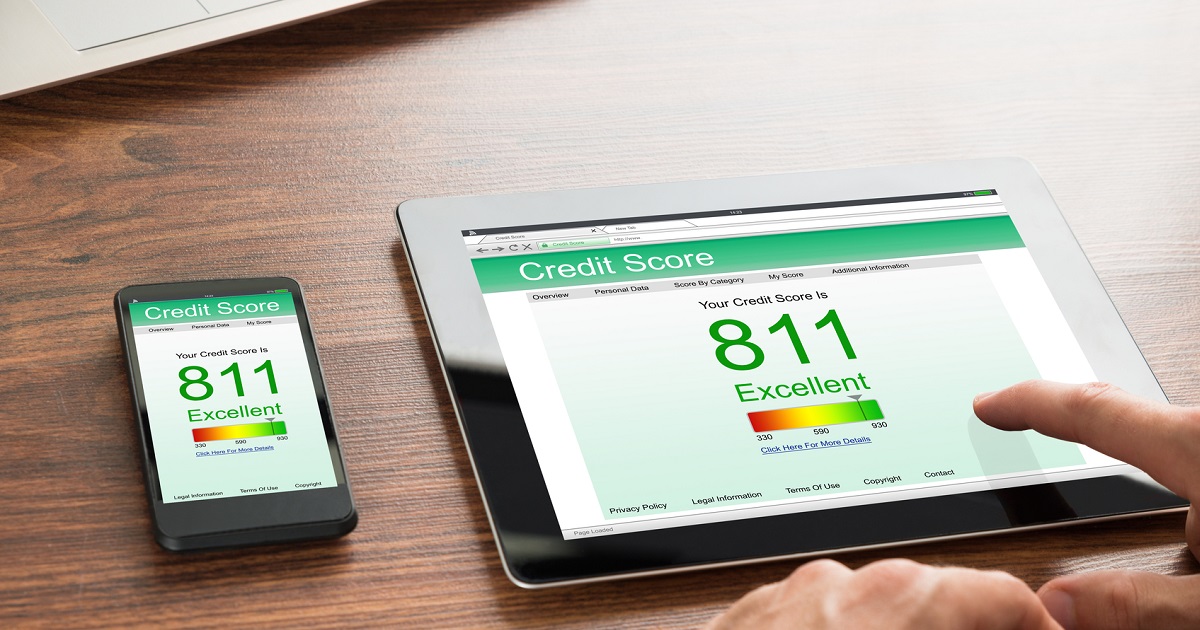

The most important information on the credit bureau report is really your credit score, and you want it to be as high as possible. Having a high credit score will give you lower interest on loans, and make home mortgages with a zero down payment possible. You can see how important the credit score is, and why it is to your benefit to make sure that your credit score is as high as it can be.

By looking at your credit bureau report and taking the advice of a trusted financial professional you can take action to raise your credit score. This could potentially save you thousands of dollars, so take action and do it soon.

What is a Credit Bureau?

The simplest answer is that credit bureaus, like Equifax, are data collectors. Credit bureaus, also known as credit reporting agencies, do two things:

1. We compile your credit history based on your credit accounts, using your Social Security number or other identification information.

2. We provide your credit information, in the form of credit reports, to lenders and creditors to help them determine your creditworthiness. We also provide credit reports to you, so you can better understand your credit situation. Your credit history, including factors such as your payment history and your amounts owed, are used along with other factors to calculate your credit scores.

Do the three nationwide credit bureaus make lending decisions?

A frequent misperception about the three nationwide credit bureaus (Equifax, Experian and TransUnion) is that they make lending decisions. Credit bureaus provide some of the information creditors and lenders use to help them make important lending decisions. While credit bureaus collect credit information in order to make it available to certain third parties, the decision to deny or approve someone credit ultimately lies with the lender or creditor. Each lender and creditor may have its own criteria.

Where do credit bureaus get their information?

Credit bureaus use different sources for collecting information, and not all third parties report to the three major credit bureaus. This means that each of your credit reports may contain different information. Creditors keep the credit bureaus updated with your account status and payment history — two factors that contribute to your credit scores.

Speaking of credit scores, there are many different credit scoring models used by credit bureaus and other entities. As a result, your credit score may vary between the three nationwide credit bureaus — even if all of your creditors report to all three. While many do, some creditors may report to only two, one or none at all.

What types of information are on credit reports?

Credit bureaus collect the following types of information:

- Credit account information, including payment history, balance of an account, when the account was opened, date of the last activity, high credit on the account and the credit limit on the account

- Debt collections

- Bankruptcies

It’s important to note some companies may take these factors and others into consideration when evaluating your application for credit.